SMM October 22 News:

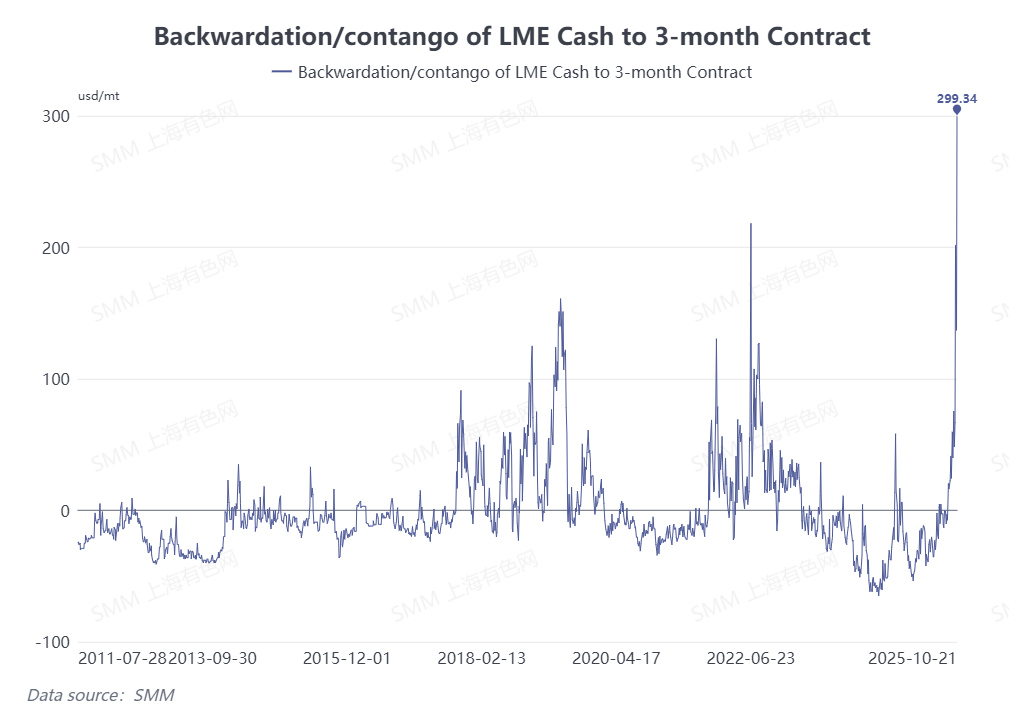

Since the National Day holiday, the LME zinc backwardation structure has surged rapidly. As of October 21, 2025, the LME zinc Cash-3M backwardation climbed to $299/mt, hitting a multi-year high, with LME outperforming SHFE. Market concerns over a "squeeze" have intensified. From a fundamental perspective, what are the underlying reasons, and what is the outlook?

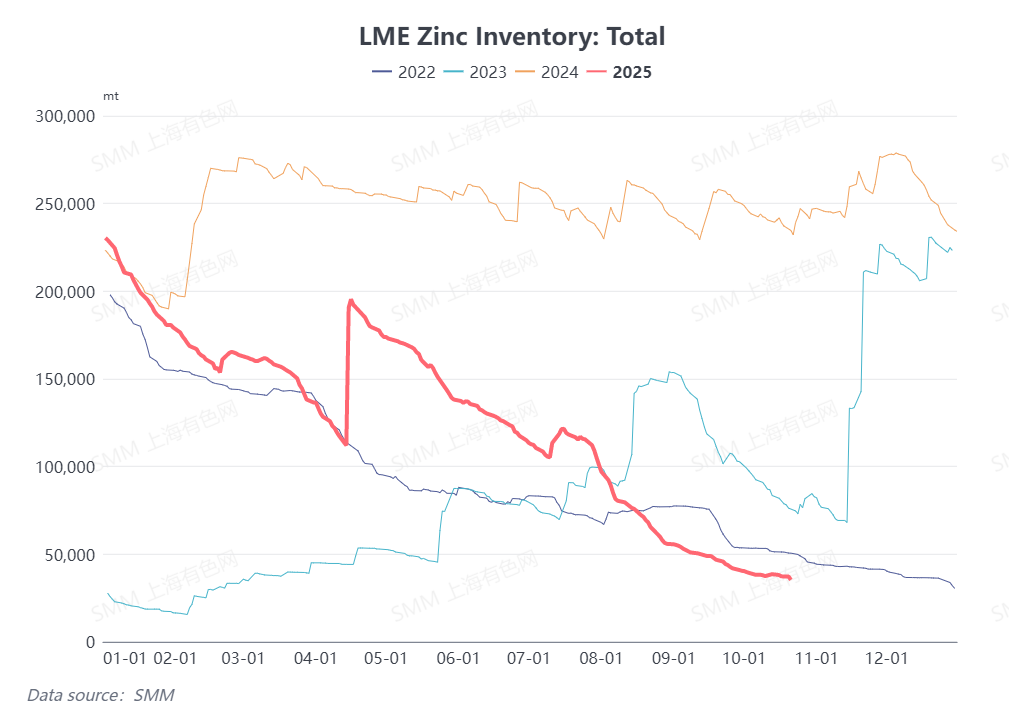

Inventory data shows LME zinc inventory currently stands at only 37,000 mt, a low since March 2023. Although the ratio of cancelled warrants is not particularly high at 35.8%, the low inventory base means the available zinc inventory for withdrawal from the LME is merely 23,000 mt, which is insufficient compared to overall overseas consumption. Meanwhile, supported by low inventories, LME zinc prices have been rising since September, again breaking through the $3,000/mt mark. Significant long positions and substantial covering pressure on short positions are further exacerbating squeeze risks.

Fundamentally, according to SMM, influenced by historically low zinc concentrate benchmarks, production enthusiasm among some overseas smelters has been low this year, with some even cutting production. Additionally, disruptions from factors like energy costs and environmental protection have led to mixed production adjustments. SMM expects overseas refined zinc production this year to be basically flat YoY. However, overseas consumption continues to grow, with higher growth rates in Southeast Asia driving continued destocking of zinc ingots in LME Singapore warehouses. The mismatch between overseas supply and demand has led to a significant decline in LME zinc ingot inventory this year, down approximately 200,000 mt from the beginning of the year, boosting the LME Cash-3M backwardation.

However, SMM believes the actual probability of a sustained short squeeze occurring is relatively small.

On one hand, besides the LME inventory system, some suppliers hold hidden stocks. High zinc prices and the strong backwardation may incentivize the delivery of some hidden stocks to LME warehouses. On the other hand, imported zinc concentrate TCs have rebounded significantly since the start of the year, and smelters that previously reduced or halted production due to environmental protection or floods are gradually resuming operations. Overseas refined zinc production is expected to increase MoM from H1, and this supply increment could partially replenish zinc ingot inventories.

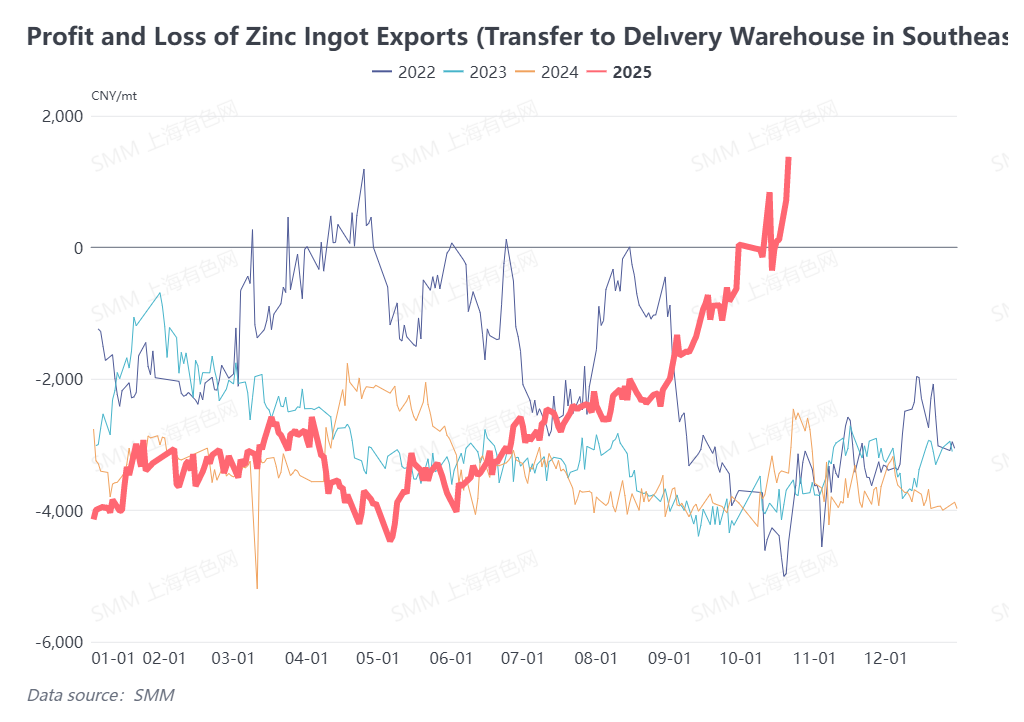

Furthermore, while LME zinc prices have been rising, the domestic Chinese zinc market has been weighed down by supply surplus and weak demand, leading to divergent performances between domestic and overseas markets, with LME outperforming SHFE. Since October, import losses for Chinese zinc ingots have continued to widen, while the export window has occasionally opened. As of October 21, the profit for exporting zinc ingots to LME warehouses reached 1,376 yuan/mt, and the spot profit for exporting to Southeast Asia was 2,016 yuan/mt. Driven by profits, some domestic suppliers have begun exporting and delivering to warehouses. The outflow of these hedged export volumes might supplement LME zinc inventories, casting doubt on the likelihood of an actual LME zinc squeeze, warranting close monitoring of future zinc ingot exports.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research and decision-making. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)